In a bid to attract millennials, Life Insurance Corporation (LIC) of India has improved its customer service experience and upgraded its online services. The results are already showing.

As of October 31, of about 10 million policies sold by LIC in 2019-20 (FY20), 2.2 million were to people aged between 18 years and 25 years, 2 million to people aged between 25 years and 30 years, and 1.7 million to people aged between 30 years and 35 years.

Millennial is a term loosely applied to people born between mid-1980s and 2000, reaching adulthood in early 21st century.

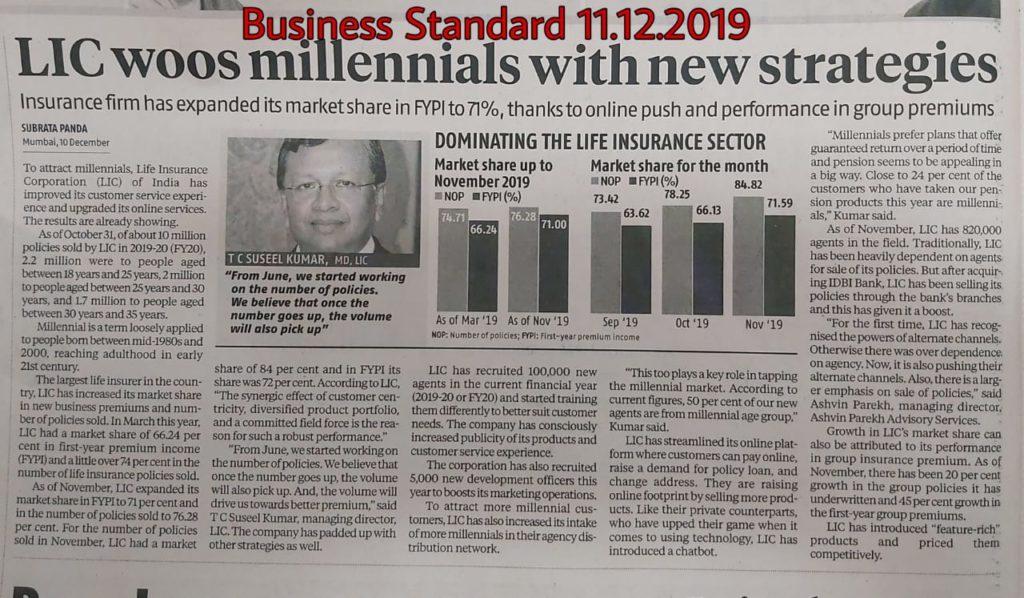

The largest life insurer in the country, LIC has increased its market share in new business premiums and number of policies sold. In March this year, LIC had a market share of 66.24 per cent in first-year premium income (FYPI) and a little over 74 per cent in the number of life insurance policies sold.

As of November, LIC expanded its market share in FYPI to 71 per cent and in the number of policies sold to 76.28 per cent. For the number of policies sold in November, LIC had a market share of 84 per cent and in FYPI its share was 72 per cent.

According to LIC, “The synergic effect of customer centricity, diversified product portfolio, and a committed field force is the reason for such a robust performance.”

“From June, we started working on the number of policies. We believe that once the number goes up, the volume will also pick up. And, the volume will drive us towards better premium,” said T C Suseel Kumar, managing director, LIC.

The company has padded up with other strategies as well.

LIC has recruited 100,000 new agents in the current financial year (2019-20 or FY20) and started training them differently to better suit customer needs. The company has consciously increased publicity of its products and customer service experience.

The corporation has also recruited 5,000 new development officers this year to boosts its marketing operations.

To attract more millennial customers, LIC has also increased its intake of more millennials in their agency distribution network.

“This too plays a key role in tapping the millennial market. According to current figures, 50 per cent of our new agents are from millennial age group,” Kumar said.

LIC has also streamlined its online platform where customers can pay online, raise a demand for policy loan, and change address. They are increasing their online footprint by selling more products. Like their private counterparts, who have upped their game when it comes to using technology to better customer experience, LIC has introduced a chatbot.

“Millennials prefer plans that offer guaranteed return over a period of time and pension seems to be appealing in a big way. Close to 24 per cent of the customers who have taken our pension products this year are millennials,” Kumar added.

As of November, LIC has 820,000 agents in the field. Traditionally, LIC has been heavily dependent on agents for sale of its policies. But after acquiring IDBI Bank, LIC has been selling its policies through the bank’s branches and this has given it a boost.

“For the first time, LIC has recognised the powers of alternate channels. Otherwise there was over dependence on agency. Now, it is also pushing their alternate channels. Also, there is a larger emphasis on sale of policies,” said Ashvin Parekh, managing director, Ashvin Parekh Advisory Services.

Growth in LIC’s market share can also be attributed to its stellar performance in group insurance premium. As of November, there has been 20 per cent growth in the group policies it has underwritten and 45 per cent growth in the first-year group premiums.

LIC has introduced “feature-rich” products and priced them competitively.

“There was a general perception that LIC premium rates were not competitive. So, the new products that we have launched are very competitive in terms of pricing,” said Kumar.